U.S. Bank Shield Card Review 2026: 0% APR and Cash Back on One Card

The U.S. Bank Shield offers 0% intro APR on purchases and balance transfers plus ongoing cash back rewards — a combination most 0% APR cards skip. Full 2026 review.

Most cards built around a 0% intro APR period earn nothing on spending — they're pure debt payoff tools. The U.S. Bank Shield is a bit different: it pairs a solid 0% intro window with ongoing cash back, so it has a role even after the intro period ends.

Whether that combination is better than a dedicated 0% card depends on your situation.

Card Details

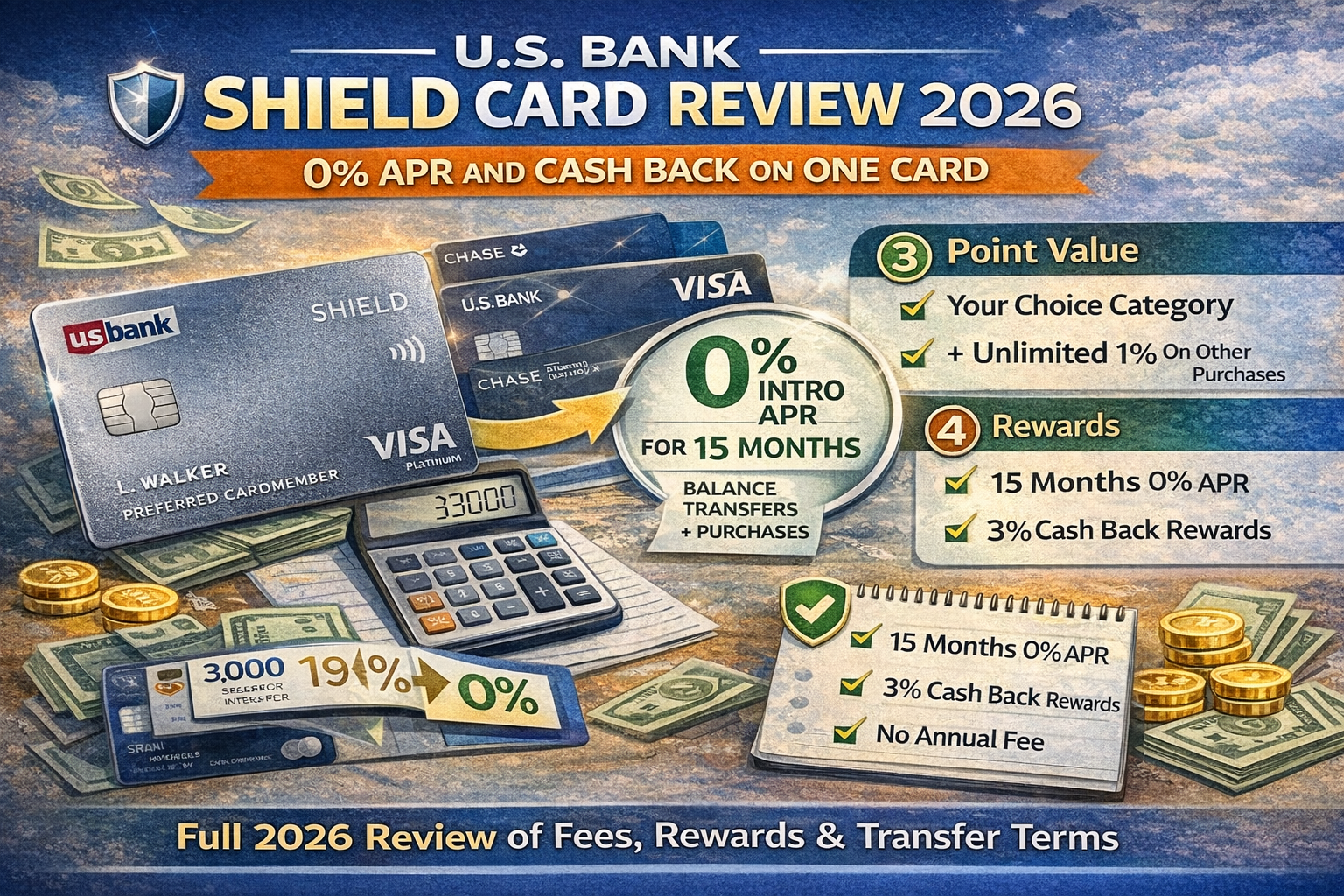

Annual fee: $0

Intro APR on purchases and balance transfers: 0% for 15 billing cycles from account opening

Balance transfer fee: Either 3% of the amount or $5, whichever is greater (introductory rate); standard rate applies after

Regular APR: Variable, currently in the 18–29% range

Rewards: Up to 3% cash back in a category of your choice, plus unlimited 1% on other purchases (category selection available through U.S. Bank account)

Foreign transaction fee: 0%

Track the U.S. Bank Shield on CardCurator

Get alerts for credits, bonus milestones, and annual fee renewals — free.

The 0% APR Window

At 15 billing cycles (roughly 15 months), the Shield's intro period is shorter than the Wells Fargo Reflect or Citi Diamond Preferred, which both offer 21 months. If maximizing the 0% window is the only goal, those cards are better tools.

Where the Shield stands out is the 3% balance transfer fee, which is lower than the 5% charged by most competitors. On a $5,000 transfer:

- Shield: $150 fee

- Citi Diamond Preferred: $250 fee

- Wells Fargo Reflect: $250 fee

That $100 difference matters if you're doing a single moderate-sized transfer and want to minimize upfront cost.

The Rewards Layer

After the intro period, the Shield continues to earn:

- 3% cash back in one category you choose (options typically include gas stations, restaurants, grocery stores, online shopping, or travel)

- 1% cash back on everything else

This makes the Shield a reasonable card to keep long-term — not best-in-class for rewards, but functional. The 3% category is competitive with dedicated cash back cards for that specific category, as long as the category you choose is one of your higher spending areas.

Compare this to a card like Wells Fargo Active Cash, which earns 2% flat on everything. If your chosen category represents most of your spending, the Shield wins. If your spending is diversified, the flat 2% is simpler and often better overall.

How It Compares to the Wells Fargo Reflect

| U.S. Bank Shield | Wells Fargo Reflect | |

|---|---|---|

| Annual fee | $0 | $0 |

| Intro APR window | 15 months | 21 months |

| Balance transfer fee | 3% ($5 min) | 5% ($5 min) |

| Ongoing rewards | 3% chosen category + 1% base | None |

| Foreign transaction fee | 0% | 3% |

Choose the Reflect if you need more time to pay down a larger balance and want to minimize the monthly payment required.

Choose the Shield if you want a lower transfer fee, your balance is smaller (so a shorter window is fine), and you want to keep the card earning rewards after the debt is paid.

Compare U.S. Bank Shield vs Wells Fargo Reflect →

How It Compares to the U.S. Bank Smartly

U.S. Bank's other no-fee card, the U.S. Bank Smartly, earns 2% cash back on everything with no category selection required. It doesn't have a 0% intro APR offer. If you're past the debt payoff phase and just want a simple rewards card from U.S. Bank, the Smartly is cleaner. If you want the 0% intro window and are willing to pick a category, the Shield wins in year one.

Compare U.S. Bank Shield vs U.S. Bank Smartly →

Who This Card Makes Sense For

Good fit if:

- You have $1,000–$4,000 in high-APR debt and want a lower transfer fee

- A 15-month payoff window is achievable for your balance

- You want a card that continues earning after the debt is cleared

- You travel internationally (no foreign transaction fee)

Consider alternatives if:

- Your balance is large enough that you need 21 months to pay it off

- You prefer the simplicity of a flat 2% card

Bottom Line

The U.S. Bank Shield fills a specific niche: lower balance transfer fee than the market standard, shorter intro window than the longest-window cards, and ongoing rewards that make it useful past the payoff period. If your balance is moderate and you want the card to pull double duty as a rewards card going forward, it's worth a look.

Compare the Shield:

- U.S. Bank Shield vs Wells Fargo Reflect

- U.S. Bank Shield vs U.S. Bank Smartly

- U.S. Bank Shield vs Citi Diamond Preferred

Track your debt payoff and rewards on Card Curator.