Citi Diamond Preferred Review 2026: Best Card for Balance Transfers?

The Citi Diamond Preferred offers 0% intro APR for 21 months on balance transfers — one of the longest on the market. Full 2026 review: fees, transfer terms, and who it actually makes sense for.

The Citi Diamond Preferred is not a rewards card. It earns no points, no cash back, nothing. What it offers instead is one of the longest 0% introductory APR periods available — and for someone carrying high-interest credit card debt, that can be worth significantly more than any signup bonus.

Here is the honest picture of what this card does, what it costs, and when it makes sense.

Card Details

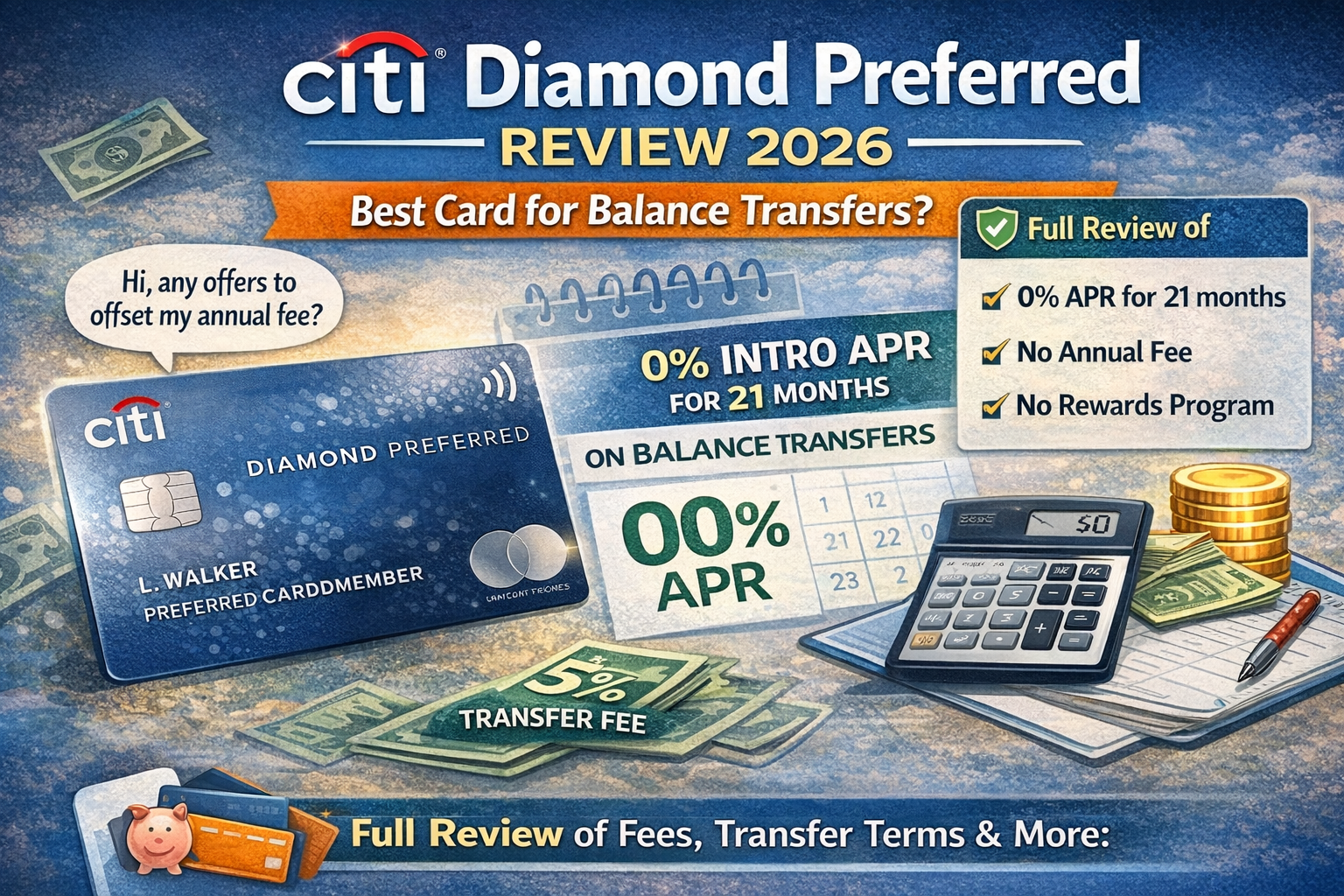

Annual fee: $0

Intro APR on balance transfers: 0% for 21 months from first transfer (transfers must be completed within 4 months of account opening)

Intro APR on purchases: 0% for 12 months from account opening

Regular APR: Variable, currently in the 17–28% range depending on creditworthiness

Balance transfer fee: 5% of each transfer, minimum $5

Foreign transaction fee: 3%

Track the Citi Diamond Preferred on CardCurator

Get alerts for credits, bonus milestones, and annual fee renewals — free.

The Balance Transfer Math

The pitch is straightforward: move high-interest debt to this card, pay 0% for 21 months, and pay it down without interest compounding against you.

The cost to do that is the balance transfer fee — 5%, or $50 per $1,000 transferred. If you're moving debt from a card charging 24% APR, the break-even is quick. On a $5,000 balance at 24% APR, you'd pay roughly $1,200 in interest over 21 months. The 5% balance transfer fee costs $250. The math strongly favors the transfer.

Where it gets complicated:

You need a plan to pay it off. The 0% period is finite. When it ends, the remaining balance starts accruing interest at the regular variable rate — which can be high. Divide your balance by 21 to find the monthly payment required to clear it before the rate resets.

The transfer fee adds to the balance. If you transfer $5,000, the fee ($250) is added to the card balance, so you're starting at $5,250. Factor that into your payoff math.

Minimum payments won't cut it. The required minimum payment is much lower than what you'd need to pay off the balance before the intro period ends. Don't rely on the minimum.

How It Compares to the Wells Fargo Reflect

The other major long-0%-APR card is the Wells Fargo Reflect, which offers 0% intro APR for 21 months on both purchases and balance transfers, with a potential extension. The Reflect's balance transfer fee is also 5% ($5 minimum) after the first 120 days.

For most balance transfer situations, the two cards are nearly identical in cost and value. The main difference:

- Citi Diamond Preferred has a longer purchase APR intro period relative to Reflect's standard terms

- Wells Fargo Reflect offers a slightly more user-friendly mobile app and stronger fraud protections in some users' experience

Neither earns rewards, so this is purely a debt payoff decision.

Compare Citi Diamond Preferred vs Wells Fargo Reflect →

How It Compares to the Citi Simplicity

Citi's other no-rewards card, the Citi Simplicity, is positioned similarly but with one difference: no late fees and no penalty APR. If you're worried about missing a payment, that's meaningful protection. The Simplicity typically has a shorter intro APR period than the Diamond Preferred, so if your priority is maximizing the 0% window, the Diamond Preferred usually wins.

Compare Citi Diamond Preferred vs Citi Simplicity →

Who This Card Is For

Good fit if:

- You have $2,000+ in credit card debt at 18%+ APR

- You can commit to a monthly payoff plan for 21 months

- You qualify for the card (generally requires good to excellent credit)

Not a good fit if:

- You want rewards on ongoing spending (get a rewards card instead)

- You're unlikely to pay off the balance before 21 months (the rate reset will hurt)

- You need to transfer from another Citi card (Citi doesn't allow transfers between its own products)

The Trap to Avoid

The most common mistake with balance transfer cards is treating the 0% period as a reason to keep spending on the card. New purchases during the intro period also get 0% for 12 months — but once that period ends, payments are applied to the lowest-APR balance first. If you've accumulated new purchases and haven't paid off the balance transfer, you can end up in a worse position than when you started.

Use this card for the balance transfer. Buy things on a different card — ideally one with rewards.

Bottom Line

The Citi Diamond Preferred is a focused tool. It does one thing well: gives you 21 months to pay off transferred debt without interest. At $0 annual fee, it costs nothing to get and the math on a substantial balance almost always favors the 5% transfer fee over continued high-interest payments. If you have high-APR debt and a realistic payoff plan, this card is worth considering.

See how it stacks up:

- Citi Diamond Preferred vs Wells Fargo Reflect

- Citi Diamond Preferred vs Citi Simplicity

- Citi Diamond Preferred vs Chase Slate

Track your cards and payoff progress on Card Curator.