How to Compare Credit Cards: 5 Things That Actually Matter

Most credit card comparisons focus on the signup bonus. Here are the five factors that actually determine which card wins for your wallet — and how to run the math yourself.

Move from reading into a concrete card decision.

Start with compare pages when you are down to a shortlist. Use statement review later only if this article maps to spending you already have and you want a final validation step.

Most credit card comparison articles lead with the signup bonus. That's the wrong place to start. A signup bonus is a one-time event. The card you choose will affect what you earn on every purchase for the next several years. Getting that decision right matters a lot more than chasing an extra 10,000 points.

Here are the five factors worth actually examining when comparing credit cards.

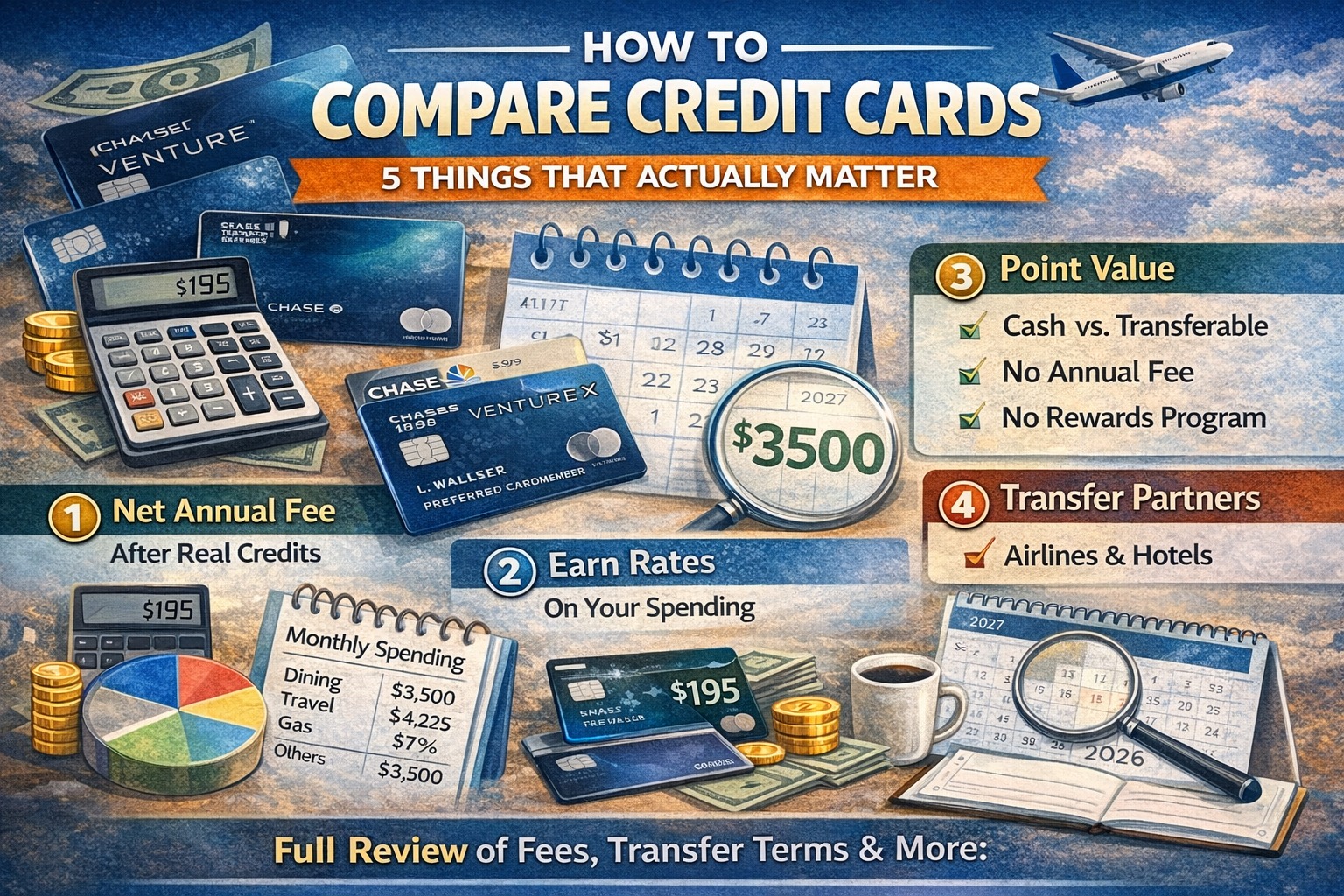

1. Net Annual Fee (Not the Sticker Price)

The annual fee printed on a card is almost never the real cost. Most cards — even expensive ones — include credits that offset the fee if you use them.

How to calculate the real cost:

Take the annual fee, subtract the value of credits you will actually use (not credits that require you to change your behavior), and that's your net cost.

Example: The Chase Sapphire Reserve has a $795 annual fee. But it includes a $300 travel credit that applies automatically to travel purchases, and a $300 dining credit. If you travel and eat out, those two credits alone bring the effective fee down to $195. The Capital One Venture X at $395 comes with a $300 travel portal credit and 10,000 anniversary points (worth ~$185 at conservative valuation), making the effective fee around $10.

The trap: Credits tied to specific portals, specific merchants, or monthly caps often don't get fully used. Be honest about which ones you'll actually claim.

Compare Chase Sapphire Reserve vs Capital One Venture X →

2. Earn Rates on Your Actual Spending

A card that earns 4x on dining is worthless to someone who cooks at home. Before comparing cards, look at your last three months of spending and categorize it.

Common categories and the cards that lead them:

| Category | Top earners |

|---|---|

| Dining | Amex Gold (4x), Chase Sapphire Reserve (4x), Citi Strata Premier (3x) |

| Groceries | Amex Gold (4x at U.S. supermarkets), Blue Cash Preferred (6%) |

| Travel | Chase Sapphire Reserve (4x direct hotels, 10x Chase Travel), Amex Platinum (5x flights) |

| Gas | Citi Strata Premier (3x), U.S. Bank Altitude Go (4x) |

| Everything else | Citi Double Cash (2%), Wells Fargo Active Cash (2%), Chase Freedom Unlimited (1.5%) |

The math that matters: multiply your monthly spend in each category by the earn rate. Do that for each card you're comparing. The card with the highest annual earnings (minus the net annual fee) is typically the winner.

3. Point Value: Not All Points Are Equal

A card that earns "3x points" sounds better than one that earns "2% cash back" — but only if those points are worth more than 1 cent each.

The key distinction is whether a card earns transferable points or fixed-value points:

- Transferable points (Chase Ultimate Rewards, Amex Membership Rewards, Capital One miles, Citi ThankYou Points) can be sent to airline and hotel partners, where they often unlock redemptions worth 1.5–3+ cents per point.

- Fixed-value points (most airline miles redeemed at face value, portal-only points) are worth exactly 1 cent each, period.

If you compare a card earning 3x transferable Chase points to a card earning 2% cash back, the actual comparison is: 3 × (value per point) vs. 2 cents. At 1.5 cents per point, the Chase card wins. At 1 cent per point, they're equal. The comparison depends entirely on how you plan to redeem.

If you always redeem for cash back or statement credits, treat transferable points as worth ~1 cent and compare accordingly. If you're willing to learn partner transfer programs, they can be worth significantly more.

4. Transfer Partners (If Relevant)

If you ever fly on a major airline or stay at Hyatt, Marriott, or Hilton, transfer partners are worth understanding.

A transferable points currency lets you move points to airline and hotel programs — typically at a 1:1 ratio — to book award travel. This is how you access 2–3 cent per point redemptions.

Why it matters for comparisons: Two cards might earn the same number of points per dollar, but if one has access to Hyatt (a high-value partner) and the other doesn't, they're not equivalent for award travel purposes.

Chase Ultimate Rewards → Hyatt, United, Southwest, British Airways, Singapore, and others

Amex Membership Rewards → Delta, Air France/KLM, British Airways, Hilton, Marriott, and others

Capital One miles → Air Canada Aeroplan, Turkish Miles&Smiles, British Airways, and others

Citi ThankYou Points → Turkish Miles&Smiles, Air France/KLM, Singapore, and others

If you have a specific redemption in mind, check whether the cards you're comparing have the partners to get you there.

5. The Second-Year Value (Not Just Year One)

Signup bonuses distort year-one comparisons. A card offering 100,000 points (worth ~$1,500) looks incredible in year one but might not outperform a simpler card in year two.

For any card with an annual fee, ask: Does this card justify its fee from ongoing benefits alone, ignoring the signup bonus?

If the answer is no, and you got the card purely for the bonus, factor in whether you'll keep it, downgrade it (if the issuer allows), or cancel it before the next annual fee hits. Some issuers let you product-change to a no-fee version of the card, preserving your credit history without paying a fee.

When Point Redemptions Don't Make Sense →

Putting It Together

A practical comparison checklist:

- Calculate net annual fee for each card (sticker fee minus credits you'll use)

- Estimate annual earnings based on your actual spending categories

- Assign a realistic point value based on how you'll redeem (1¢ for cash back, 1.5–2¢ if you use transfer partners)

- Subtract net fee from estimated annual earnings — this is your net annual value

- Pick the card with the highest net annual value

For most people comparing two similar cards, the difference comes down to one or two spending categories where the earn rates diverge, and whether the credits on a higher-fee card are genuinely useful.

Use the CardCurator Comparison Tool

CardCurator shows annual fees, current signup bonuses, reward rates by category, credits, and transfer partners side by side for any two cards you choose. It pulls live data on current offers so the bonus amounts are always up to date.

Popular comparisons to start with: